This is an opinion piece based on personal experiences and research into StartEngine, its management, vendors, and shareholders.

First Impressions

Let me rewind back to November 2015…

It was a bitter cold day in Washington DC, and boy, was I feeling it. I’d just flown in from “The Sunshine State” leaving temperatures at around 90°F, and arriving near freezing, with snow falling too. This was my second visit to DC, my first being as a 16-year-old in tow with Mum and Dad many, many moons ago when on vacation.

I had arrived in DC to attend the Crowdfunding Professional Association conference scheduled for the next day.

The following morning during the conference, and after several speakers had come and gone on stage, it was the turn of the StartEngine CEO (at the time), Ron Miller.

With a video ready to roll in the background. Miller then went on to say:

“This video generated 27 million dollars.”

The $27 million Miller referred to, were in fact Expressions of Interest, also known as Reservations during a Test-the- Waters campaign, so no real investments had taken place at the time.

My first impression was not a good one.

I glared at him. He glared back.

And then the video began…

It was a video about Elio Motors, hoping to develop a 3-wheeled car. The $6,800 (now electric and $14,900 according to their website) three-wheeled car is designed principally for commuting and was expecting to get an estimated 84 miles per gallon. Elio were in the throes of raising capital at the time using the REG A+ exemption and had launched a Test-the-Waters campaign on the StartEngine platform. The actual REG A+ raise itself did manage to raise almost $17M.

Today, a whole 10+ years later, Elio still has not brought this car to market, and looking at their website, it appears that it is barely functional. One can’t help but be suspicious of a slow rug-pull going on over these past few years. This article sheds some light on the situation back in 2021: Elio Motors Took Millions in Customer Deposits, Never Delivered Car.

StartEngine’s Valuation Game

StartEngine’s journey from a $120 million valuation in 2019 to a staggering $1.3 billion just a few years later raises several red flags. The company’s management appears to have strategically manipulated its share price, benefiting insiders at the expense of retail investors.

During 2019, StartEngine initially raised funds through the TruCrowd portal at a valuation of $120 million. Over the next 2 years, it conducted seven more crowdfunding campaigns (some on their own platform and the others on TruCrowd), each time increasing the valuation without substantial justification, with one increase going from $786B to $1.3B in several months. By the time they reached a valuation of $1.3 billion, and at a share price of $25,management had sold millions of dollars’ worth of their own shares to largely unsuspecting retail investors.

The increase in share price culminated in a raise at $25 per share, which critics argue was unjustifiable. The previous round’s valuation was a mere $786 million just months earlier, suggesting a drastic and unsupported spike in valuation.

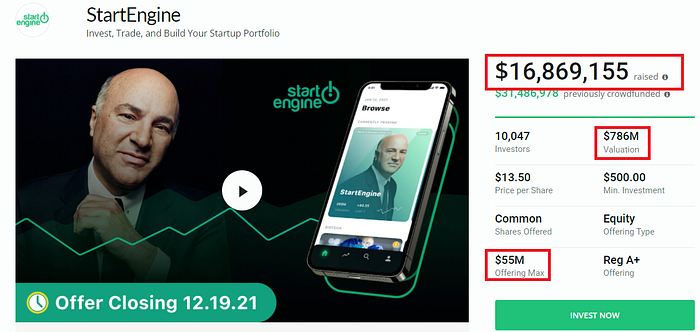

Interestingly, only one campaign out of them all managed to reach its funding target, although that raise only targeted a couple of hundred thousand dollars. All others failed, and in some cases, really badly. For example, their REG A offering which closed on Dec 19th, 2021, had a funding goal of $55M and only managed to raise $16,869,155

This was followed up by a REG A raise targeting $75M during 2022 at a valuation of $1.3B, which managed to raise a total of $24.5M by November, 2023. (Crowdfundinsider)

It appears that StartEngine are really not very good at crowdfunding. Probably good at manipulation though, and as we’ve seen, not so good at actually raising $’s for themselves.

Strategic Stock Splits and Market Positioning

Adding to the complexity of StartEngine’s valuation is its strategic decision to implement a 20-for-1 stock split. This maneuver effectively lowered the price per share to $1.25 from $25, making it more accessible to a broader range of investors. This move is typically seen as a strategy to increase liquidity and attract more retail investors, which aligns with StartEngine’s goal of democratizing investment in startups (Hubtas).

The stock split also signals potential future plans for an Initial Public Offering (IPO). For StartEngine to list on NASDAQ, it would need a minimum bid price of $5 per share. This suggests that the company might aim for a valuation of at least $5.28 billion to meet the listing requirements (Hubtas).

Regulatory Compliance and Corporate Governance

StartEngine has also made significant changes to its corporate structure and governance to enhance compliance with federal and state laws. These changes were unanimously approved by the Board of Directors and the majority of stockholders, reflecting strong internal support for the company’s strategic direction (StartEngine).

Despite these efforts, the company’s transparency and management practices remain under scrutiny. Insiders, including employees and senior officers, are prohibited from trading on StartEngine Secondary to avoid conflicts of interest and market manipulation. However, earlier investors still face restrictions, which adds another layer of complexity to the company’s trading practices (StartEngine).

The Aftermath for Retail Investors

Today, StartEngine’s share price reflects a valuation of around $250 million, a far cry from the inflated $1.3 billion valuation at which insiders sold their shares. This dramatic decrease in value has left retail investors with little to nothing of value. The management’s actions during the period of inflated valuations, where they sold off significant holdings, have resulted in significant financial losses for those who bought in at the higher prices.

A Closer Look at Financial Performance

StartEngine’s financial performance over the past few years reveals a pattern of aggressive growth strategies coupled with questionable financial health. In 2021, the company reported sales of $29.08 million, a significant increase from $12.57 million in 2020. However, despite this growth in revenue, the company’s operating income and net income remained in negative territory, with losses widening year-over-year (markets.businessinsider.com).

The balance sheet also shows a substantial increase in total liabilities, rising from $2.32 million in 2020 to $7.29 million in 2021. This increase in debt, coupled with a negative net income, raises concerns about the company’s long-term financial stability and its ability to deliver on its promises to investors.

Future Prospects and Investor Sentiment

As StartEngine looks to the future, its path to an IPO remains uncertain. The company’s need to achieve a valuation of at least $5.28 billion to meet NASDAQ listing requirements suggests that an IPO is still years away. Meanwhile, the company’s efforts to increase share liquidity and attract new investors through stock splits and other strategic maneuvers will likely continue.

Investor sentiment, however, remains mixed. While some view StartEngine as a pioneer in democratizing investment in startups, others are wary of its aggressive valuation tactics and the significant financial losses incurred by retail investors. The company’s ability to rebuild trust and demonstrate sustainable growth will be crucial in determining its long-term success.

Conclusion: Pioneers or Con Artists?

StartEngine’s rise in the equity crowdfunding space is marked by significant achievements and equally significant controversies. The dramatic increase in valuation, strategic stock splits, and regulatory maneuvers suggest a company adept at navigating the financial landscape to its advantage. However, the lack of substantial justification for valuation increases and the potential exploitation of retail investors cast a shadow over its practices.

As StartEngine moves closer to its goal of going public, it will need to address these concerns to maintain investor confidence and truly democratize investment opportunities. Whether viewed as pioneers or con artists, StartEngine’s story is a compelling case study in the complexities and potential pitfalls of equity crowdfunding.

Looking Ahead: Lessons for the Future

As we move into mainstream equity crowdfunding, there are important lessons to learn from the mistakes of others. Firstly, the customer is still king and even more so when they are the ones feeding your very existence. Ignoring their voices is a common sight, even among the new breed of equity portals and platforms. Campaign creators and issuers with ideas will always be around in huge numbers attempting to pitch their wares. However, the backers and investors won’t unless you treat them with fairness and listen to their voices.

While others make critical mistakes, and in some cases crumble into oblivion, upcoming platforms and portals must always look out for the real customers — the project creators and issuers who bring their ideas, and more importantly, the investors who bring the real money to the table.